Keeping a lump of cash aside to pay provisional tax on your Inland Revenue due dates can be challenging for any business, especially if you have cashflow issues and need money on hand. For some companies and sole traders, tax pooling is the perfect solution.

What’s tax pooling?

Being part of a tax pool provides more flexibility on when you pay provisional tax to Inland Revenue, rather than being tied to the IRD’s deadlines.

How it works

IRD-approved intermediaries such as TMNZ or Tax Traders transfer money to Inland Revenue on your behalf. Once the pool has made the payment to IRD, it is considered ‘tax paid’.

All you have to do is keep up with your payments to the pool or purchase tax payments with a finance charge. This allows you to better make payments to help your cashflow.

Tax pools provide flexibility, allowing you to overpay when you have a bit more money and giving breathing room when things get tight. Overpayers help other businesses in the pool that need more time to make their payments.

The pros of tax pooling

You’ll avoid IRD’s penalty charges and use of money interest (UOMI) charges for late payments as the pool will always make time-stamped payments for you.

If you haven’t paid enough tax to meet your provisional tax liability, tax pools typically charge lower interest rates for purchasing tax payments than those charged by IRD.

You can dip into your tax pool payments and use them as an emergency line of credit if you’re short on cash, as long as you top up the money later.

If you take money out of the pool, you’ll be charged a lower rate of interest than those charged by the banks.

In short, tax pools can give you more control over your provisional tax obligations. Talk to us today to see if tax pooling is the right fit for you.

Got March balance dates?

Remember your first provisional tax instalment is due this month, on August 28. Here’s a breakdown of your key dates this year:

1st instalment: 28 August

2nd instalment: 15 January

3rd instalment: 7 May

Mixed-use asset rule change explained

April 1 marks a significant change in the GST tax treatment of mixed-use assets.

Taxpayers can claim 100% of GST for expenses relating to the income-earning use of a mixed-use asset, for example, the cost of advertising a holiday home online.

However, working out GST claims for expenses relating to both the income-earning and private use of the asset has been more difficult to establish.

In the past, a complex calculation has been needed to apportion GST expense claims relating to both income-earning and private use.

As of this month, GST calculations for mixed-use assets have been simplified. You no longer need to use the old method and general apportionment and adjustment rules will apply instead.

Remember, if you have a mixed-use asset, such as a boat, bach, or plane, please keep records on how and when it is used for business or private purposes.

If you’re unsure about these changes, give your adviser a call.

Your 12-point checklist to stay ahead on tax

1.Contracts

Have you invoiced retentions that don’t need to be paid until next year? If they are payable this tax year, they will be classed as taxable income for 2023-24. Unsure? Talk to us as your tax adviser.

2.Employee expensesand holiday pay

Holiday pay, bonuses, redundancy payments, and long service leave owed to employees can be claimed this year if you have committed to them at year-end and pay them within 63 days of the balance date.

Also, ensure holiday pay has been calculated correctly to avoid time-consuming revisions once the tax year is over. Find more information here or visit the Employment NZ website.

3.Credit notes

Take stock of credit notes issued to customers after the balance date. You may be able to apply them to the current tax year and reduce your taxable income.

4. Expenses

Find out if you can prepay expenses before March 31 for items such as stationery, postage, and courier charges to claim deductions sooner.

5. Debtors

Before the end of March, review your debtors and make a list of any outstanding bad debts. Ensure your records show you’ve taken reasonable steps to recover bad debts. Bad debts written off before March 31 can often be claimed as a deduction.

6. Fixed assets

If you’re not using some of your assets, you may be able to write them off.

7. Tax losses (carryforward, offsets and subvention payments)

Set to make a loss in the current financial year or have tax losses from prior years? Talk to us as soon as possible about carryforwards, loss offset elections and subvention payments.

8. Discounts for prompt payment

If you’ve offered prompt payment discounts over the tax year and maintain a discount reserve, this might be deductible. Make sure you keep clear records about any discounts.

9. Repairs and maintenance

Thinking about doing repairs or maintenance? Get it done before the year-end to ensure you get your deductions sooner. Consider software development and improvement costs as part of this.

10. Dividends and imputation credits

Review your dividend payments for the year by March 31. Imputation credit accounts mustn’t have a debit at the year-end, or you could be hit with penalties.

Also, review deemed dividends (for example, overdrawn shareholder current accounts with no interest charged).

11. Stock

Dispose of obsolete stock by year-end or write it down to its net realisable value (the lesser of cost or market value).

If your stock is worth less than $10,000 and your turnover is less than $1.3 million for the year, you won’t need to include stock movements for tax purposes.

12. FBT

Review all FBT items. Have you taken account of possible exemptions? The FBT March quarter return is the year’s last quarterly return and will most likely require a wash-up calculation.

GST and the new Airbnb/Uber Tax

GST and the new Airbnb/Uber Tax

If you offer accommodation or ride share services in New Zealand via an electronic marketplace (e.g., Airbnb or Uber), new GST changes will impact on you from 1 April 2024, although the National Party has stated it will repeal the change if they are elected to Government in October this year.

At present, providers of these services are not subject to GST if their turnover is below the $60,000 GST registration threshold. However, the Tax Bill which passed through select committee on 2 March 2023 now imposes GST on accommodation and transport services provided through electronic marketplaces, regardless of whether or not the owner of the property or the driver is registered for GST. The Bill is likely to be passed into legislation in the coming weeks.

What is changing

The Taxation (Annual rates for 2022-23, Platform Economy, and Remedial Matters) Bill (No 2) creates a category of services called ‘listed services’ which incorporate all commercial, short-stay and visitor accommodation (such as Airbnb, Bookabach and Booking.com), as well as all ride-share and food and beverage delivery services (such as Uber, Ola and Lyft).

This change means the marketplace operator is deemed to be the supplier of the services and is required to collect and return GST at 15% on all services provided to end-users through their marketplace.

The supply between the marketplace operator and a GST registered property owner or driver will be zero rated for GST. For example, Sarah is GST registered and rents out a property via the Airbnb marketplace for $100 a night. Airbnb is deemed to be the party supplying the accommodation and adds GST to the nightly rate, therefore charging guests $115. Airbnb pays the $15 GST to the Inland Revenue. The transaction between Airbnb and Sarah is zero-rated, therefore Sarah includes $100 as a zero-rated supply in her GST return.

If the property owner or driver is not GST registered, the marketplace operator deducts 8.5% input tax from the taxable supply (referred to as a flat-rate credit), and passes that 8.5% credit to the property owner or driver. The flat-rate credit is intended to approximate the amount of GST that the property owner or driver could claim as input tax if they were GST registered. Therefore, if Sarah was not GST registered, she would receive a credit of $8.50 (8.5% of $100) from the marketplace. The marketplace will return net GST of $6.50 to the Inland Revenue ($15 – $8.50). Current commentary is unclear on how Sarah treats the credit in her income tax return and no doubt detailed guidance will be provided once the legislation is passed.

What are the exemptions

Large commercial enterprises who offer over 2000 nights of short-stay accommodation per year via a marketplace enter into an agreement with the marketplace operator to opt-out of the new rules and allow them to continue being responsible for their own GST obligations.

In a nutshell

Ultimately there should be no change to GST registered property owners’ or drivers’ back pockets, while non-registered property owners or drivers may have additional income to declare in their tax returns due to the flat-rate credit. Although non-registered property owners or drivers could voluntarily register for GST, this may not be the ideal solution for property owners.

If you require assistance in understanding how you will be impacted by this new GST rule, please contact us.

Fundamental GST changes coming your way

Fundamental GST changes coming your way

Ever since GST was first introduced in 1985, businesses have become very familiar with various aspects of GST which have been fundamental to meeting their GST compliance obligations.

Under the guise of “modernising GST” the Inland Revenue is introducing a number of invoicing and record keeping changes that will apply from 1 April 2023.

These changes have two stated purposes being:

To reduce the cost of doing business; and

To support e-invoicing and electronic record keeping.

As part of these changes, there will be a number of key terminology changes:

Tax Invoice will become Taxable Supply Information

Debit/ Credit Note will become Supply Correction Information

Buyer-created Invoice will become Buyer-created Taxable Supply Information.

From 1 April 2023, there will no longer be a requirement to keep a single physical document holding the supply information. Instead, various information contained in your accounting system and contract documents may be used to support the numbers used in your GST returns. The thresholds for when you need to hold Taxable Supply Information will also increase.

Whilst clearly the way businesses transact has changed since GST was first introduced, the changes from 1 April 2023 could potentially add additional compliance costs for some businesses as their support for various supplies may need to come from multiple sources/ locations, rather than the old tax invoice.

The above changes are not compulsory and businesses can continue to issue tax invoices and credit/debit notes as they have in the past. You may however find over time that some of your suppliers will change what documentation they produce and you will need to ensure you have sufficient other Taxable Supply Information documents to support any GST claims made.

The Inland Revenue have stated they will be issuing more information on this, leading up to the date these changes come into effect.

In the meantime, if you have any questions on how the GST changes will affect you, please contact us.

GST Special Alert 2023

New rules on GST invoicing apply from 1 April 2023. These changes have been designed for 21st century business record-keeping and modernise invoicing rules in place since 1986, based on paper-based record-keeping systems.

The rules are permissive, so businesses can issue current tax invoices without falling foul of the new rules. However, this doesn’t mean you can ignore them. Your suppliers and customers may introduce changes to their systems stemming from the new rules. You need to be ready to cope with receiving ‘taxable supply information’ in different formats, as opposed to a ‘tax invoice’.

It’s important to note there are no changes to the imposition or calculation of GST – these new rules only relate to information requirements.

A major component supporting the GST system’s integrity is the provision of prescribed information about taxable supplies contained in a tax invoice. Considerable changes have occurred in business practices relating to transactional information and technology since GST’s introduction over 35 years ago, and the new rules reflect this. They are less prescriptive, allowing the way supply information for goods and services is created, provided, and retained to be determined as part of normal record-keeping processes.

From 1 April 2023 businesses must retain a minimum set of information relating to transactions, and are no longer required to issue a ‘tax invoice’ for GST purposes. Don’t forget, however, that normal commercial and contract law still require invoices and record-keeping requirements. Invoices must still be used to notify the customer of their obligations for a taxable supply, but from 1 April 2023 an invoice will not need to meet the old prescriptive requirements such as displaying the words ‘tax invoice’.

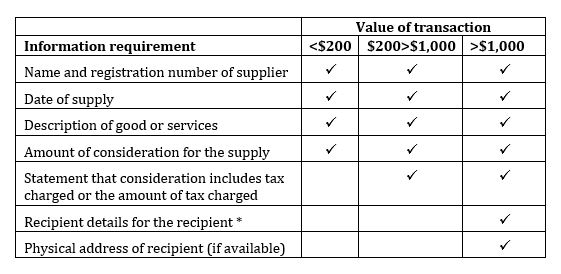

‘Taxable supply information’ is effectively replacing tax invoices and must be retained and able to be provided.

The information required is dependent on the value of the transaction.

* Recipient details require the name of the recipient and one or more of the following:

Address of a physical location

Telephone number

Email address

Trading name other than the name of the recipient

New Zealand business number (NZBN)

Website address

Requirements around credit and debit notes are similarly revised. Formal GST credit and debit notes will no longer be required, however information known as ‘supply correction information’ must be retained. This includes information on inaccuracies corrected such as incorrect descriptions of goods or services, places/times of supply or suppliers/customers.

You must provide supply correction information where the taxable supply information previously provided to a recipient has an incorrect amount of GST, or where you included the incorrect amount of output tax in a GST return. You must provide this information by a date agreed between you and the recipient, or if no date is agreed, within 28 days of the date of the taxable supply information that contained the mistake.

Where the GST shown in the taxable supply information is greater than the eventual GST charged due to a prompt payment discount or an agreed discount which are part of usual business terms, you won’t have to provide the supply correction information.

What about Buyer-Created Tax Invoices?

New buyer-created taxable supply information follows the same criteria as the normal taxable supply information, depending on the value of the transaction, i.e. whether it’s less than $200, or up to $1,000 etc. More importantly, you no longer need Inland Revenue approval to use buyer-created taxable supply information (previously required for buyer-created tax invoices). However, both parties to a buyer-created taxable supply arrangement must agree that only the recipient will provide buyer-created taxable supply information and you must record the reasons, if they are not part of the normal terms of business between the parties.

Note any existing Inland Revenue approvals to use buyer-created tax invoices are not affected.

Even though the new rules still allow ‘tax invoices’ to be issued after 1 April 2023, it is important to make sure you think about:

Your accounts payable processes. Do your systems or staff automatically reject invoices which don’t have the words ‘tax invoice’ on them? If so, review this as your suppliers (and customers) may update their systems for the new rules. You may receive invoices after 1 April 2023 which don’t have these words on the invoice. The same will apply for credit notes, debit notes and buyer-created tax invoices.

Your information management systems. Review your systems to ensure supplier and customer databases can handle the taxable supply information requirements, especially recipient information (e.g. physical address and NZBN options).

Reviewing arrangements with suppliers and customers where buyer-created invoicing is more appropriate. Where you are entering into new buyer-created taxable supply information arrangements, you will need to retain the correct records (including copies of the agreements).

The time of supply rules. Certain transactions will have a different time of supply to the date the invoice is created. From 1 April 2023, the time of supply must be included in taxable supply information.

Training your staff on the new rules, including on what is required to support GST input tax deductions. As well as a refresher on GST, it will also give you the opportunity to review supplier/customer arrangements and ensure all business/trade terms are current and comply with the new rules.

Progressing towards e-invoicing if you haven’t already. These new GST invoicing rules have been introduced to cater for technology and business processes. More efficient invoicing processes could benefit your business.

April 2023 is not that far away. Please contact us to help you assess what your business may need to do before then!

GST invoicing changes are coming!

New rules modernising GST invoicing and record-keeping requirements will apply from 1 April 2023. The key change is removing the requirement to issue and hold a “tax invoice” document (which meets certain prescribed requirements on details required), and instead having GST requirements met provided specific GST information is held through various business records, for example commercial invoices or agreements.

Tax invoices will be replaced by taxable supply information (TSI). This is a set list of information that must be provided to any GST-registered customers within 28 days of the date of supply. Information over and above current tax invoice requirements includes:

the ”date of the supply” — when the time of supply is triggered, rather than the current tax invoice requirement of the date on which the tax invoice is issued

for supplies over $1,000, the TSI must include the recipient’s physical address (if that information is available).

For supplies over $200 it will become mandatory to issue TSI to GST-registered customers within 28 days of the date of supply, and for supplies made to non-GST registered persons you have 28 days from when the customer requests the information.

Other favourable changes include the increase of the low-value threshold from $50 to $200 where limited taxable supply information is required and the removal of IRD approval for issuing buyer-created tax invoices (to be replaced by written agreements between parties to confirm self-billing).

The new invoicing rules have been designed with the intent that businesses issuing valid tax invoices now would not have to make any changes to comply with the new rules, however all businesses will need to be aware of the changes to ensure their business processes can manage the new GST requirements (i.e. accepting invoices which don’t have the words “tax invoice” on them).

We will have more information for you about the changes over the coming months.

Residential Rental Property Tax

There are many tax implications when investing in residential property in New Zealand. Property investment and understanding the impact of current tax laws and their application is rather complex now, Please seek professional advice when you are unsure of the implications, as mistakes can be costly!

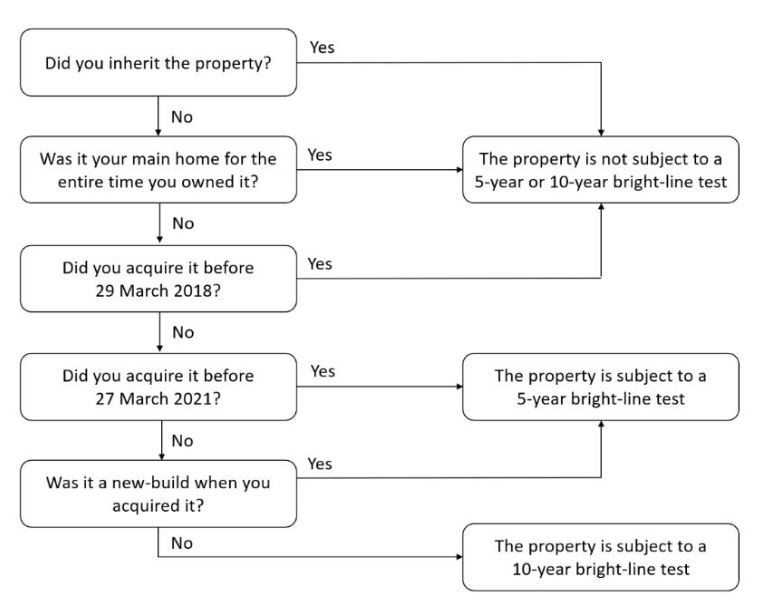

The Brightline test

For sale and purchase agreements that become unconditional on or before 27 March 2021, the “old” Brightline test is applied.

All other properties with a settlement date on or after 28 March 2021 will be subject to the revised Brightline test.

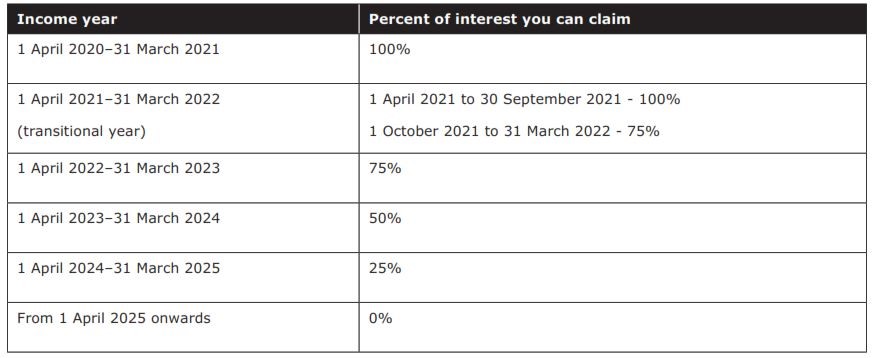

Interest deductibility

Property purchased on or after 27 March 2021 – interest can be claimed up to and including 30 September 2021. After that, no interest can be claimed.

Property purchased on or before 26 March 2021 can claim the percentages outlined below.

Ringfencing Rules

Previously, losses from rental properties can be offset against other sources of income (wages, salary, business income), thereby reducing an individual’s tax liability.

From 1 April 2019 any loss made from a rental property will be ring-fenced. It will be contained within the rental itself and used on a ‘portfolio basis’. The two types of property income losses can be offset against are:

Future residential rental income from across your portfolio; or

Any taxable income on the sale of residential land.

Any losses left over will stay ring-fenced to be used in the future against this type of income, ie future residential rental income only and cannot be offset against other personally derived income to lower your overall tax payable, potentially giving rise to a refund

What Expenses can be Claimed

Income from residential property rental should not be declared for GST, and any costs shouldn’t be claimed for GST, either.

Property-related expenses

Rates

Insurance

Property management fees

Repairs and maintenance

Travel to and from your property for inspections and repairs

Financing expenses

Mortgage repayment insurance

Loan fees

Interest on mortgage*

Legal and consulting fees

Legal fees incurred when buying a rental property (if less than $10,000)

Legal action to recover unpaid rent

Costs for evicting a tenant

Preparation of a tenancy agreement

Accountancy fees

Valuation fee to obtain a mortgage (but not insurance valuations)

Legal fees for selling the rental property (if your total legal fees are less than $10,000)

Non-deductible costs

Mortgage repayments (except interest*)

Interest subject to the new interest deductibility rules announced 23 March 2021

Repairs and maintenance, if it increases the value of the asset

Insurance valuations

Legal fees for selling the rental property (if your total legal fees exceed $10,000)**

Advertising the sale of a rental property**

Real estate commission**

With the government’s new housing plan announced on 23 March 2021, claiming interest against residential rental income has become severely restricted. If you’re purchasing a rental property, assume that interest cannot be claimed.

For properties acquired on or after 27 March 2021:

Legislation has passed that extends the bright-line test from five years to 10 years on residential property.

The Government intends for the bright-line test to remain at five years for new builds and will be consulting on what a new build is soon.

Legislation has passed that introduced a ‘change of use’ rule. If the sale of your property is subject to the bright-line test, and you don’t use a property as your main home for 12 months or more, you will be required to pay income tax on a proportion of the profit made through the property increasing in value.

The Government has proposed that residential property investors will not be able to offset the costs of the interest they pay on loans to purchase residential property as an expense against their taxable income. A consultation will be held about this, with any law expected to come into effect from 1 October 2021.

Employment Matters

Sick leave entitlement changes

The recent passing of the Holidays (Increasing Sick Leave) Amendment Act increased the employee sick leave entitlement from 5 to 10 days per year. The change comes into effect on 24 July 2021. The day in which the employee’s sick leave increases is based on their next entitlement date and not automatically from 24 July.

Median wage increase

The median wage increased from $25.50 to $27 gross per hour from 19 July 2021. This has implications for employers who may be intending to employ staff on an essential skills visa or residence visa

Covid-19 travel policy

The current pause in the trans-Tasman bubble and Wellington’s recent alert level change serves as a timely reminder that businesses need to plan for on-going travel uncertainty. Make sure you have an updated travel policy in place that covers what to do when an employee’s work or personal trip is extended, and the steps that employees should take when travelling in the bubble.

Covid-19 vaccinations and employees

As the vaccination programme rolls out across New Zealand, you might be wondering what your obligations are as an employer. Make sure you are clear on what you can and cannot do when it comes to Covid-19 vaccinations and your workers. Employment New Zealand has released some guidelines to help employers understand their role in the vaccination process. The guidelines can be found on their website together with a one-page PDF for your workplace.

New Trust Disclosures

With the introduction of the 39% tax rate for individuals from 1 April 2021, the Inland Revenue is increasing the information it collects from trusts to assess compliance with the new tax rate and to monitor how trusts are being used.

Trust disclosure obligations

The additional information that needs to be included in a trust’s tax return (from the 2022 tax year) includes:

name, IRD number and date of birth of beneficiaries, settlors and those with power of appointment and removal of trustees

financial statements

details of settlements

details of distributions to beneficiaries

Non-active trusts, charitable trusts, Maori authority trusts, and New Zealand trustees of foreign trusts do not need to provide this additional information.

Increased disclosure obligations to beneficiaries

In addition to the above, from January 2021, trustees need to disclose the following trust information to all beneficiaries, including parents/guardians where the beneficiary is under 18:

that they are a beneficiary

name and contact details of all trustees

that they can request a copy of the trust deed and the financial statements

Trustees can choose not to provide requested information to beneficiaries provided the request has been reasonably considered. The beneficiary does not need to be told the reason for not providing the information.

Change to definition of settlor

There has also been a change to the definition of a settlor. A beneficiary with a current account greater than $25,000 will now be deemed to be a settlor if a market interest rate or Inland Revenue’s prescribed interest rate is not charged. This can have implications for the beneficiary such as student loan repayments and social assistance.

Purchase Price Allocation Rules

If you are planning to buy or sell a business, you need to be aware of the new purchase price allocation rules that apply to business asset sales as well as commercial property sales. The new rules took effect from 1 July 2021 and impact the way parties allocate the agreed purchase price between tangible and intangible assets.

The new rules overcome the issue of vendors and purchasers allocating different prices to the same asset resulting in a tax mismatch for Inland Revenue. Under the new purchase price allocation rules, the parties either have the option of agreeing an allocation which will be applied for tax purposes by both parties, or if no agreement is made, then a legislative process applies for determining the allocation.

There is a de minimis threshold for transactions where the total consideration is less than $1 million, or if residential land and chattels are involved, the threshold is for consideration of less than $7.5 million.

Reinstatement of Depreciation on Commercial Buildings

Since the 2012 income year the depreciation rate for commercial and industrial buildings had been reduced to 0%. Following the Government’s raft of Covid-19 support measures, depreciation can now be claimed on commercial and industrial buildings from the beginning of the 2021 income year. The reinstatement will mean commercial and industrial buildings are now depreciated at 2% diminishing value or 1.5% straight-line. Residential buildings continue to have a 0% depreciation rate.

If you had previously depreciated your commercial or industrial building prior to the 2012 income year, you must continue to depreciate the building from the 2021 income year. Alternatively, if you own a commercial or industrial building that you held prior to the 2012 income year and you had previously elected not to depreciate, you must continue not to depreciate.

Covid-19 Business Support

This lockdown was announced at 17 August 2021 and has triggered three of the government’s existing policies – Resurgence Support Payment, the Covid Wage Subsidy, and the COVID-19 Leave Support Scheme. The terms ’employee’ and ‘business’ below include sole traders and shareholder-employees.

For businesses which expect a loss of at least 40% revenue as a result of this lockdown

• To be paid as a two-week lump sum

• Can only be used for wages, not general operating costs

• $600 per week for each full-time employees

• $359 per week for each part-time employee

Applications expected to open on 20 August from Work and Income NZ.

Resurgence Support Payment (RSP)

The RSP is available if a business incurs a drop of 30 percent in revenue over 7 days, compared with 7 days in the last 6 weeks as a result of the Alert Level increase. For commonly owned groups, the whole group needs to be eligible before each entity can claim the RSP.

For businesses which expect a loss of at least 30% revenue as a result of this lockdown

• To be paid as a lump sum

• Can be used for general operating costs

• The amount is to be the lower of:

• $1,500 plus $400 per full-time equivalent employee (up to 50 FTEs), or

• Four times the actual revenue decline experienced by the business

Leave Support Scheme (LSS)

The LSS provides a two-week lump sum payment of either $585.80 per week for full-time workers, or $350 per week for part-time workers, who must self-isolate and cannot work from home.

For employers to help pay employees who cannot work from home while self-isolating

• $585.80 per week for full-time employees

• $350.00 per week for part-time employees

Short-Term Absence Payment (STAP)

The STAP provides a one-off (once per 30 days) $350 payment for workers who must miss work due to a COVID-19 test and cannot work from home. Further information is available on the MSD website.

Does the new 39% tax rate affect you?

The new 39% marginal rate that applies to all employment income over $180,000 is now in force. Consider how the new rate will affect you and your business.

The 39% tax rate and…

Trusts?

From now on, you’ll need to disclose a lot more information to Inland Revenue in your annual trust tax returns. The additional information will provide the Government with information on how trusts are being used, particularly with the introduction of the new 39% tax rate. As part of their annual income tax return, trustees will now have to disclose:

Financial accounting information, including profit and loss statements and balance sheet items

Loans to related parties

Information on distributions and settlements made during the income year

Names and details of settlors from prior years

Names and details of each person who, under a trust deed, has the power to appoint/dismiss a trustee, to add/remove a beneficiary, or to amend the trust deed.

FBT?

A new Fringe Benefit Tax (FBT) rate of 63.93% will apply for all-inclusive pay above $129,681 and the single rate and pooling of non-attributed fringe benefit calculations. The 42.86% rate for non-attributed benefits will no longer apply. Talk to us about your current FBT profile and we can review it together.

RWT and RLWT?

If you earn interest, this will be taxed at 39% (RWT) from 1 October 2021. If you’re selling property covered by the bright-line test, Residential land withholding tax: (RLWT) will increase from 1 April 2021 to 39% (except where the vendor is a company).

Beneficiary income from a trust?

If you receive beneficiary income from a trust let us know if you’d like to know more about your tax position.

Property or shares?

If you are looking to purchase assets such as property or shares, or already have such investments, it would be prudent to assess your overall investment strategy so that it meets your commercial and personal goals, including your tax profile.

Such investments are able to be held in companies or a trust, which have tax rates of 28% and 33% respectively, however on distribution to individuals in most cases the individual’s tax rate will effectively be applied.

A strong note of caution – the main reason for any restructuring of your investments should not be due to any perceived tax benefits arising out of the restructure. Any restructuring should be focused on achieving key objectives such as successful commercial, risk, succession, and asset protection outcomes. Talk to us and we

can review and assist you with planning to meet your objectives.

Superannuation contribution tax?

Time to check whether you have employees whose Employer Superannuation Contribution Tax (ESCT) and Retirement Savings Contribution Tax (RSCT) rate threshold exceeds $216,000. The tax rate for these has risen to 39% (as of 1 April 2021).

Additional employment income?

The tax change applies to all employment income over $180,000 a year, including bonuses, back pay, redundancy, and retirement payments. As an employer, take account of when additional remuneration to employees may affect their tax obligations and make sure tax is deducted correctly.

From Airbnb to boarders: What’s new for property owners?

Renting your home or bach online?

If you rent a property for short periods, you need to know your tax commitments. New rules announced last May come into force this financial year.

Here’s what you need to know:

2,500

If your tax due at end of year is more than $2,500, you’ll have to pay provisional tax instalments the following year.

60,000

If you earn more than $60,000 a year from your taxable activities, you must register for GST. If you earn less than $60,000 a year, you can choose to register for GST.

If you have the choice, think carefully about whether registering for GST is best for you. Once you’re registered, there are ongoing requirements (such as recordkeeping, invoicing and filing returns) and when you sell your property or stop providing short-stay accommodation you’ll probably have GST to pay.

Unsure if being GST registered is the right way to go? Give us a call for advice.

Hosting boarders at your place?

You need to choose between the standard-cost method and the actual-cost method to work out the income you make from boarders so you know how much tax to pay.

The standard-cost method keeps things simple because when your income from a boarder is equal to or below standard costs, it’s tax exempt. You can also claim standard costs instead of claiming on actual expenses. The weekly standard cost per boarder has just been changed to $186/week for the 2019/20 tax year. What does it include? Food and household bills, gifts, and entertainment and activities you provide for your boarder. You’ll also need to calculate your annual hosting and transport costs.

Five or more boarders? You have to use the actual-cost method. Up to four boarders? You can choose to claim actual costs instead of standard costs. Under the actual cost method all your income from the rental is assessable income and must be declared. To use this method, you need to:

Keep full records of your actual income

Keep full records of your expenses

Fill out an IR3 annual tax return to return income and claim actual expenditure incurred.

If you don’t complete a return of income by the due date for filing, IRD will assume you picked the standard cost method.

Either way, keep your records!

Because you may not know until the end of the tax year whether you’ll want (or be able) to use the standard-cost method, make sure you keep full records. Jot down the number of weeks you had boarders, the total income from boarders, cost of capital improvements or rent paid, kilometres you travelled transporting them, and any other related expenses.

What’s new in 2020?

Partnership Law gets a makeover:

The Partnership Law Act 2019, which governs business partnerships …

New kilometre rate for claiming motor vehicle expenses

Are you using your car for business purposes? It’s timely to outline the process for claiming tax on your work vehicle expenses.

If you’re using a vehicle for business purposes, you can claim tax back on expenses.

If you use the vehicle only for business, you can claim the full running costs. If you use the vehicle for any personal travel, you’ll need to separate the running costs of your vehicle between business and private use.

There are two ways to calculate the business usage:

Actual costs mean keeping accurate records, including details of private and work-related expenses. You also need to show the reasons for business travel and the distances involved.

Use a logbook to record all business trips and then calculate an actual business use percentage for each period. Or keep a logbook for at least 90 consecutive days to work out the business use of your vehicle, which you can then use for the next three years (as long as the nature of the business varies by less than 20% over that time).

Once you have the business proportion, you can use the Inland Revenue’s kilometre rates to work out how much you can claim:

Tier One is calculated as a combination of the vehicles’ fixed and running costs. It applies for the business portion of the first 14,000 km travelled by vehicle in a year.

Tier Two accounts for running costs only and applies for the business portion of any travel in excess of 14,000 kms.

To make claiming your business usage easier, make sure you record odometer readings at the end of every year to help determine your business mileage vs personal mileage.

If you are a company and provide vehicles to staff (including yourself!), you will need to make sure you’ve got your fringe benefit tax position right. Talk to us as there are exemptions that may apply for specific types of vehicles or where restrictions are placed on the use of company owned vehicles.

Four-week checklist to keep tax time low-stress

Week 1: First things first

Talk to your accountant or bookkeeper. They’ll tell you what you need to do before 31 March including what you can claim for and what you can’t. Remember, tax time is busy for them too, so the more prepared you are, the smoother the process, and the better the result.

File your return on time. Don’t waste your hard-earned cash on unnecessary interest and penalties. Get your accounts up to date, tidy up loose ends and file on time.

Week 2: Your assets and stock

Review your inventory. The value of your stock affects your business’s taxable profit. Do a meticulous stocktake before year-end. Get rid of any out-of-date or damaged items and write them off.

Extra assets on board? Year-end is the time to ditch surplus assets. If you can sell them, great, otherwise write them off.

Week 3: Your spending

Sooner rather than later. If you’re planning to buy any new equipment or assets, do it on or before 31 March (rather than 1 April) to reduce your taxable income and gain a full month’s depreciation.

Got invoices and receipts for your expenses? It can be tricky to keep track of everything so if you’re not already, go digital. Scanning receipts and saving electronic invoices in the cloud saves time and space.

Week 4: Your staff

Payroll up to date? Now’s the time to check your payroll system only includes current staff and that all their details are correct. Ensure former staff don’t have access to company systems.

Remember tax on bonuses: Special bonuses this time of year can be a great way to reward and motivate staff, just remember to get the tax right on any lump sums made. Also keep in mind any bonuses for the current year, and holiday pay or long service leave paid out within 63 days after 31 March can be deducted against your current year income.

Rental losses ring-fenced from 1 April 2019

The new law on ring-fencing rental losses is now in force, which means:

In most cases ring-fenced deductions will be carried forward and can only be used against residential rental or sale of property income in future years.

Property investors will, in most cases, no longer be able to reduce their tax liability by offsetting residential rental property deductions against their other income, such as salary or wages, or business income.

The new rules apply from the start of the 2019-2020 income year and apply to:

Mainly rental properties but can also include other residential land.

Individuals, partnerships, trusts, look-through companies and close companies.

Own a rental property? We’re happy to talk you through your tax implications so you don’t get caught out.

Pay your taxes by cheque?

Five new ways to do it.

If you normally write a cheque to pay for your taxes, it’s time to decide how you will pay in the future. As of 1 March 2020, Inland Revenue will no longer be accepting cheques. By the end of the last financial year (June 2019), only around 5% of payments received by Inland Revenue were by cheque, so they made the call to phase them out.

Here are five faster, cheaper and safer ways to pay your taxes:

Pay securely by direct debit using a debit card or credit card through myIR. Login and register at www.ird.govt.nz

Make payments using online banking – contact your bank to find out how

Use credit or debit cards to make online payments at ird.govt.nz/pay

Visit Westpac and pay your taxes in person by EFTPOS or cash

If you’re overseas, pay using a money transfer service. Search “make a payment” at ird.govt.nz

New GST on low-value imported goods

Overseas businesses selling goods valued at $1,000 or less online to New Zealanders are now required to register for, collect …

Property sales on IRD radar

Buying or selling a home? You’ll now need to provide your IRD number as part of the transaction process. The change will allow IRD to know who’s flipping owner-occupier homes on a regular basis, and better enforce the existing law that ensures people pay tax on the profit. The move won’t impact the rules around who’s required to pay tax on investment property though.

Own residential property? Take note!

In an effort to level the playing field between property investors and home buyers, a new law ring-fencing rental losses looks set to come into effect on 1 April 2019.

It means you’ll no longer be able to offset tax losses from your residential properties against other income (e.g. salary or wages, or business income).

However, the losses will be able to be used in the future when the properties are making profits, or if you are taxed on the sale of land.

Need more information? Give us a call.

April Tax News

ACC and Student Loan rate changes from 1 April:

The Student Loan Scheme annual repayment threshold increases …

Get ready for the end of the tax year!

While sorting your end of year tax paperwork sounds about as fun as spilling coffee on your keyboard, once it is done, it’s done – and now’s the time.

With not long until year end, we encourage you to spend a few minutes this week reading our top tax tips plus the latest changes you need to be aware of in 2019.

10 smart year-end tax tips

Fill your drawers: Can you stock up on stationery, postage and courier bags before 31 March? Claim now and save.

Staff expenses: If you owe employees holiday pay, bonuses, long service leave or redundancy payments, you can claim for these now – as long as they are paid within 63 days of the balance date

Can you fix it? If you’ve got any significant maintenance or repairs on the cards, do it before year end and save on tax.

Turn fun into savings: Do you know which entertainment expenses you can claim 100% of? It’s worth finding out – ask us if you need clarification.

Look at your fixed assets: Do you have any you’re no longer using or don’t plan to use in the future? If so, you may be able to write off the book value.

While you’re at it, check your stock: Look at your stock as well, especially obsolete stock. There may be an opportunity to write some of this off as well – check with us on what could be done in this area.

Income boost: Earnt a lot more this year? Consider making a voluntary provisional tax payment.

Logging car use? Remember to jot down your odometer reading at year end and if you’ve kept a logbook of business and personal use, mileage and costs, good work!

Home office: It’s also a good time to review what home office expenses may be available for deduction, especially your home office. We can help with calculating this.

Saving time saves money! Accountants are required to ask for information to comply with AML – DIA obligations plus the IRD may ask you, via your accountant, for extra information in relation to your EOY tax. Having your identification and tax documents collated and correct saves your accountant time, which saves you money, so get started this week.

What’s new in the world of tax?

Payday filing

We have mentioned this in the past, but don’t forget payday filing for employers is compulsory from 1 April 2019. Please contact us if you need any help with complying with the new process and rules.

No more cheques for IRD

Do you send post-dated cheques for tax payments? It’s time to go digital!

From now on you’ll need to use online banking to make future-dated payments as the IRD no longer accepts post-dated cheques. Plus, if you’re one to put your tax payments in the Inland Revenue’s dropboxes, you’ll now have to head to an IRD office reception area during office hours to do so.

Writing off bad debt? Get your ducks in a row

If you’re expecting a tax break from writing off bad debt, you may also expect to hear from the IRD asking you to prove the debt is, in fact, bad. A new ruling means the IRD could request evidence of any steps you took to recover the debt (before writing it off) and proof there is no reasonable likelihood the debt will be paid. So, get your paperwork in order!